|

Sales Tax Rounding |

|

| Show/Hide Hidden Text |

|

Sales Tax Rounding |

|

| Show/Hide Hidden Text |

Some authorities suggest that one should "round-up" sales taxes. This will assure that you are never "shortchanged" by not charging enough for tax.

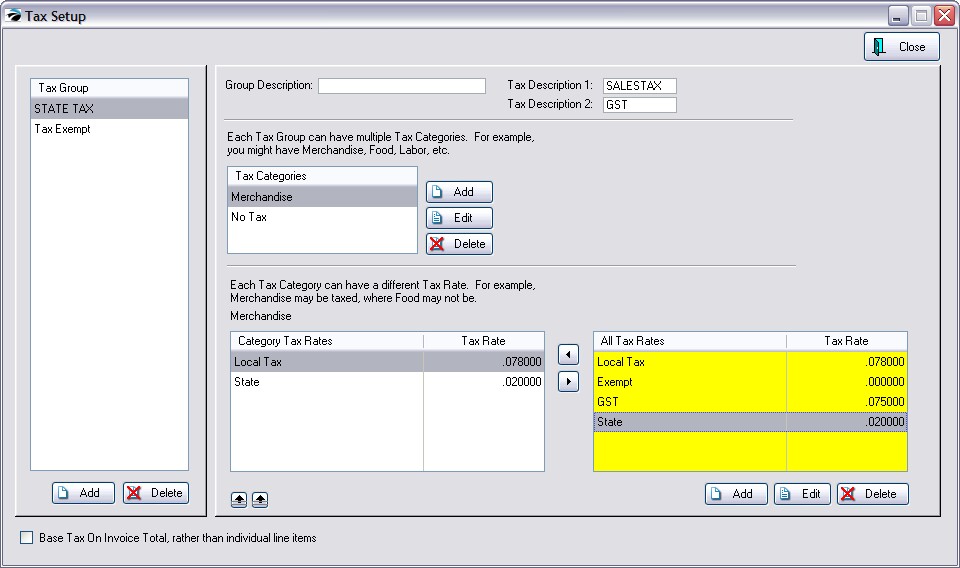

Note: If you are using two tax rates (e.g. State Tax and City Tax) as separate calculations per inventory item, you should NOT use this option. Rounding is done per tax rate and the combined tax total will cause GL Transactions to be out of balance.

|

| Click to see larger picture |

You should check with your state tax authority for guidance, but most states allow businesses to round taxes any way they want. Since most states compute the sales tax on total gross sales and not on actual sales tax collected, businesses may occasionally "over collect" tax and keep the difference.

Here is a simple example.

Suppose you charge 5% sales tax and sell an item for $.48.

The tax to be collected is $.024 which conventional rules will round down giving you $.02 for tax. If this item were sold 100 times, then you would have $2.00 collected in taxes.

The State, however, sees gross sales of $48.00 (.48 x 100 customers) and tax liability of $2.40. You have undercharged taxes and are short changing yourself.

If you choose to "Round Up", using the same example above, you will collect $.03 in tax for the sale of a $.48 item or $3.00 for 100 sales of the item. Your liability is still $2.40 and your business gains $.60.